Delivering Net Zero: The UK Hydrogen Strategy - Investable or a risky business (model)?

13 min read

Aiming Hy

On 17 August 2021, the UK Government published its Hydrogen Strategy, setting out proposals to deliver its ambition for 5GW of low carbon hydrogen production capacity by 2030 for use across the economy. Alongside the strategy document, the UK Government published consultations on the design of three key elements of the proposals: the Net Zero Hydrogen Fund, a UK low carbon hydrogen standard and a hydrogen business model.

The UK Government’s policy – unlike that of most other countries in Europe – is to follow a technology neutral approach which seeks to promote all ‘colours’ of low carbon hydrogen, whether derived from electrolysis or involving carbon capture, usage and storage (CCUS) – a so-called ‘twin-track’ approach. Whilst the strategy has been broadly welcomed by industry, it has been strongly criticised by environmental groups due to its support of blue hydrogen, produced by reformation of natural gas and CCUS.

But regardless of the production process used, low carbon hydrogen is forecast to play a role in achieving the UK’s 2050 net zero target. Analysis by the Department for Business, Energy and Industrial Strategy (BEIS) suggests 250-460TWh of hydrogen could be needed in 2050. Kick-starting this industry will require a robust business model. The UK’s low carbon hydrogen market will involve highly complex and co-dependent value-chains. Careful risk allocation will be key to its success.

Chicken or egg?

One of the key challenges in developing the UK’s low carbon hydrogen economy is the ‘chicken or egg’ problem of growing supply and demand simultaneously. On one hand, the business case for producing low carbon hydrogen is limited by its comparatively higher production costs which means it cannot compete with the market prices offered for conventional, high carbon fuels. On the other, the case for using low carbon hydrogen is limited by the current low volumes available for supply and its higher price relative to conventional fuels.

This poses a novel challenge for policy makers. Previous policy intervention for renewable and low carbon electricity has only needed to focus on the supply-side, providing price certainty for generators to recoup high upfront capex costs. A ready market for electricity was assured at the right price.

In order to stimulate both supply and demand, the UK Government has identified the need to implement a hydrogen business model that offers financial support to incentivise investment in the hydrogen economy. The business model aims to enable hydrogen to compete with existing high carbon fuels from a cost perspective, thereby stimulating fuel switching and new sources of demand.

Whilst this paper focuses on the proposed business model, BEIS recognises that a range of other decarbonisation policies may be required to stimulate demand. Perhaps most importantly, carbon pricing – via the UK Emissions Trading Scheme and Carbon Price Support – will be a key tool in promoting investment in low carbon technologies. However, given the number of potential end-use applications for hydrogen, a broad range of sector specific policies will also impact demand, including the UK’s Transport Decarbonisation Plan, the Industrial Decarbonisation Strategy and the long-awaited Heating and Buildings Strategy.

Proposal for a business model

The consultation on a business model for low carbon hydrogen invites views by 25 October 2021. The Government aims to publish a response to the consultation in Q1 2022 and finalise the business model in 2022, enabling the first allocations under that model from Q1 2023.

Producer model

The Government’s proposed business model is a producer model which will provide revenue support to new hydrogen production plants under a bilateral contract for difference with a counterparty (still to be identified). This shares similarities with the contract-for-difference model deployed by the UK Government in respect of renewable and nuclear power projects and that proposed for the Dispatchable Power Agreement as part of the CCUS business models. The private contract approach is intended to provide investor certainty and to appeal to capital with a risk appetite to invest in early opportunities in the UK hydrogen market.

The intention is that, by incentivising investment in low carbon hydrogen-production, demand will develop for that hydrogen across a variety of end use applications, including heavy industry, heat, power and transport. As the hydrogen market matures, the Government aims to reduce the reliance on Government revenue support and eventually establish a hydrogen economy which is viable without subsidy. Reductions in support may be achieved through a move to a competitive bidding process, as has been seen in renewables, most notably the offshore wind sector.

Known unknowns

The consultation focuses on design questions related to price and volume risk (also known as market risk) - these are discussed in detail below. However, to be successful, hydrogen producers will also need to consider other risks The Government has indicated that producers are best placed to bear fuel input risk, construction risk (such as cost overruns), decommissioning risks (such as decommissioning being more expensive than anticipated) and the technology risk. Management of technology risk will be important, particularly given the relative immaturity of technology supply chains and the possibility that, if the plant does not produce hydrogen that meets the low carbon hydrogen standard, it will not qualify for subsidy. Whilst we consider this to be the correct risk allocation, it will mean that investors will be very focused on (i) the extent to which those risks can be passed onto contractors; and (ii) technical due diligence and monitoring, particularly for first-of-a-kind projects, recognising that contractors are unlikely to underwrite the loss of subsidy for the life of the contract.

Interface risk also will be subject to significant analysis. The majority of low carbon hydrogen production plants will depend on either a CCUS transport and storage network or a renewable power provider for their operations. Interface risks between the projects will need careful management.

The consultation leaves a number of key commercial points open, instead seeking views on issues such as contract duration, the approach to plant expansions and the allocation process.

In addition, the Government is seeking views on how the business model will be funded. The assumption in the consultation is that the cost will be passed-on to consumers; however, given the varied end-uses for hydrogen, this is more complex to design than for clean electricity. Whilst this is a wider policy question rather than something that will impact directly the terms of the contract entered into with hydrogen producers, the robustness of the funding mechanism will be a crucial point for investors and funders.

Pricing risk

The reference price

A key element of the proposal is the pricing mechanism that will be included in the contract; producers (and those financing them) need protection against the risk that, when competing with counterfactual fuels (e.g., gas and diesel), the price the producer is able to achieve does not cover the cost of producing it. Pricing will, therefore, determine the producer’s return on investment, but it will also be a key driver in the adoption of low carbon hydrogen by end users.

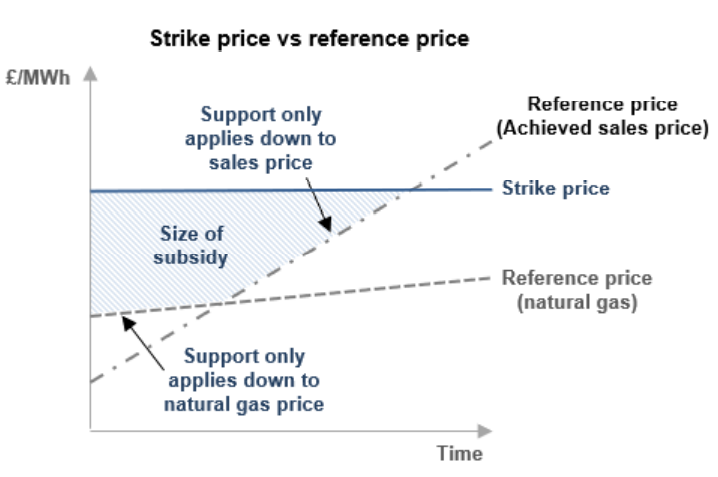

The Government’s proposed model is for a variable premium to be payable to producers, calculated as the difference between a reference price and a strike price. This is similar to the pricing mechanism in the contract for difference model for UK renewable power projects. It allows for the level of subsidy to adjust as the market matures such that, if the reference price were to rise above the strike price, then the producer would make a payment to the contract counterparty.

This approach has worked well in the power sector, where the reference price is derived from the wholesale market price for electricity. However, a single market price does not exist for hydrogen and will take time to develop. This presents a fundamental issue: what should be used as a reference price where there is no market reference?

Noting that there is no perfect solution, the Government proposes that, until a hydrogen market benchmark develops, the reference price will be the higher of the natural gas price and the ‘achieved sales price’ negotiated by the producer (shown in the diagram below). The natural gas price essentially acts as a cap to the level of subsidy to mitigate the risk of gaming (i.e., producers agreeing artificially low prices with customers) and has been selected as natural gas is the fuel from which end users will most likely switch to hydrogen.

(Source: BEIS, Consultation on a business model for low carbon hydrogen, August 2021, p48)

However, the Government wishes to include further incentives for producers to seek the highest sale price possible, enabling the subsidy from the Government to reduce over time. It will consider including additional measures such as a gainshare mechanism alongside contract price reporting in order to monitor the market. Further work is to be carried out on these proposals.

We anticipate that this minded to position will be a key area of focus in responses to the consultation. In order to implement the achieved sales price into the price calculation, price sensitive information will need to be provided by producers and end users. Industry will naturally raise questions around confidentiality, administrative burden and feasibility of proposals (for example how to account for unsold, stored hydrogen).

Finally, it is unclear how contracts will move away from this artificial reference price when a market benchmark for hydrogen emerges. New contracts can be readily drafted to include a hydrogen benchmark as the reference price. However it is unclear whether the Government intends the first contracts entered into using the artificial reference price described above to include a contractual mechanism to switch the reference price to a hydrogen benchmark once it emerges. If proposed, this would impact the wider suite of supply and offtake arrangements for a hydrogen producer.

Indexation

Industry will welcome the signal that the Government intends to index the strike price to take account of the change in the cost of inputs over time. However, how this is undertaken is subject to further analysis by the Government. The consultation invites respondents to share views on four indexation options: inflation-linked, actual input energy cost, natural gas benchmark and electricity price benchmark. Arguably a one-size fits all solution may not be feasible, and a different indexation methodology may be required, depending on whether the production method is reformation-based or electrolysis-based (given that the types of input costs materially differ between the two technologies).

End user restrictions

Another element of the business model which remains subject to further development is the extent to which the business model will attempt to differentiate between end users of the hydrogen produced. The Government notes that some existing users of hydrogen as a feedstock already place a relatively high value on hydrogen and the Government is keen to avoid the business model reducing the costs for those users, rather than incentivising new users to switch from other fuels.

Volume risk

In addition to facing pricing risk, a producer of low carbon hydrogen will also face volume risk i.e., the risk that it cannot sell some or all of the hydrogen that it produces. The consultation considers a number of policy options to manage volume risk, including availability payments and various government offtake options The Government’s preferred approach is to address this risk by way of sliding scale pricing. Under this approach the unit prices paid are higher when offtake volumes are low with the level of support reducing as offtake volumes increase. This would not eliminate volume risk, but it would reduce the volumes that a producer needs to sell in order to cover its investment costs. Under the proposals no support would be offered if volumes are zero, meaning that producers may seek to contract with multiple offtakers to mitigate this risk.

The design of the sliding scale option, including the price curve, is yet to be determined. It will need careful consideration to avoid creating perverse incentives such as plant oversizing.

A fair allocation?

The proposals will inevitably have different implications for different producers, depending on their end-user market, technology solution, inputs and offtake arrangements. The Analytical Annex to the Hydrogen Strategy notes the difference in levelised cost estimates between the different low carbon hydrogen production methods. It follows that strike prices are likely to be different for different production methods, with electrolytic hydrogen production likely to require a higher level of support due to its higher costs. How contracts are allocated, and how competition between production methods is managed therefore also will be important.

Although the consultation lacks detail, it is clear that the allocation process depends on the technology deployed. Initial CCUS-enabled hydrogen projects will be participating as part of the CCUS cluster sequencing process. Eligibility criteria for these projects was published as part of the Government’s CCUS cluster sequencing process published in May 2021 (section 4.5) and included requirements that the project be a new (not a retrofit) CCUS-enabled hydrogen production plant, be at pre-FEED stage or ready to commence pre-FEED no later than the end of December 2022 and with an expected operation date of no later than end of December 2027. Details of the allocation process for these projects will be published in the Phase 2 launch document, expected in later in 2021.

Eligibility criteria have yet to be set for other low hydrogen production methods (e.g. electrolytic hydrogen). For these projects, the Government is minded to invite project applications in 2022, followed by a bilateral selection process with successful projects taking final investment decisions from 2023.

In the medium-term, the Government expects to move to competitive allocation for all types of hydrogen project, albeit the consultation acknowledges there may need to be budget pots available for different technologies.

Is hydrogen infrastructure eligible?

Whilst small scale hydrogen pipeline and storage infrastructure may be supported as part of the project costs for the production plant, the Government’s view is that the business model is not appropriate for large scale hydrogen infrastructure. Indeed the requirement for dedicated hydrogen infrastructure will itself be subject to review, albeit with no date specified for this as yet. Although initially hydrogen production projects will be located in close proximity to centres of demand, consideration of the need for hydrogen networks and storage capacity should not be deferred too long, particularly in light of the long lead times for the development of pipelines or subterranean storage.

Beyond business models

The business model consultation is an important step towards creating a low carbon hydrogen economy in the UK. Whilst the proposals in the business model have clearly been well thought-through and are to be welcomed, there are currently too many unknowns for investors to be able to form a definitive view at this stage about the viability of the business model proposals. And although necessary, a sound business model alone is not sufficient to deliver the Government’s ambition. As noted in the Hydrogen Strategy, a number of further measures are required including a wider review of the regulatory framework for hydrogen. Industry is also likely to need better visibility of the Government’s longer-term ambition for the low carbon hydrogen market beyond 2030 for the investment in the technology, infrastructure and supply chains required to deliver a low carbon hydrogen economy in the UK.

This material is provided for general information only. It does not constitute legal or other professional advice.