Same stripes or different spots? The UK Government consults on a carbon border adjustment mechanism

18 min read

Following a previous consultation by HM Treasury and the Department for Energy Security and Net Zero and a series of “Powering-up Britain” publications released at the end of Q1 2023[1] (the “2023 Consultation”), the UK government announced that it would introduce a Carbon Border Adjustment Mechanism (“UK CBAM”) from 1 January 2027 on imports of certain carbon intensive goods. In this article, our team examines the emerging UK CBAM’s regulatory parameters, discussing how these parameters diverge from the EU CBAM, and several potential implications that may flow from such regulatory divergence.

1. Introduction

On 21 March 2024, HMRC and HM Treasury launched a joint 12-week consultation with a paper entitled “Introduction of a UK carbon border adjustment mechanism from January 2027”,[2] on which it has invited views on proposals for the design and administration of the mechanism by 13 June 2024 (the “2024 Consultation”).

The 2024 Consultation follows the implementation of the reporting obligations under the European Union’s Carbon Border Adjustment Mechanism (“EU CBAM”). The EU CBAM’s reporting obligations commenced on 1 October 2023, with importers obliged to pay tariffs from 1 January 2026. Please see our previous publication “The EU Carbon Border Adjustment Mechanism begins to bite: What does it mean for businesses and what next?”, published on 14 November 2023, for an overview of EU CBAM.[3] In addition to the EU CBAM, the 2024 Consultation points to Australia and Canada as jurisdictions which are considering equivalent measures.

In this publication we:

- consider the 2024 Consultation proposals for the UK CBAM and identify points of note; and

- discuss its current and future coverage and potential divergences from EU CBAM and the 2023 Consultation.

2. Background to a UK CBAM

In an effort to curb emissions of greenhouse gases (“GHGs”), a number of jurisdictions have implemented some form of carbon pricing, with the aim of capturing the costs of GHGs to society.

In parallel to the EU Emissions Trading System, the UK has established an Emissions Trading Scheme (“UK ETS”) whereby certain UK-produced goods are subject to carbon pricing.

Like the EU, the UK government is aware that domestic efforts to reduce emissions and decarbonise could be undermined by so-called carbon leakage (companies relocating to avoid higher carbon pricing and more stringent climate regulation whereby emissions are “displaced rather than reduced”).[4] Exporters who are subject to carbon pricing are also concerned that they may be less competitive as they pass those carbon costs on to consumers.

The UK’s current main measure to mitigate carbon leakage risk is the system of free allowances under the UK ETS given to operators in sectors viewed as vulnerable to carbon leakage, which will be protected until 2026. Reforms to the UK ETS, as set out by the UK ETS Authority in July 2023, will reduce the number of UK ETS allowances available for purchase from the government by 45% between 2023 and 2027, and from 2026 the number of free allowances will also decrease with free allowances intended to be phased out by 2030.[5]

The UK CBAM will be a measure aimed to address these concerns by extending UK domestic carbon prices to certain imported emissions generated extra-territorially and thereby “levelling the playing field”.

3. Overview of the UK CBAM and differences from the EU CBAM

3.1 How will the UK CBAM work?

The UK CBAM is a tariff paid by importers of specific emissions-intensive, trade-exposed goods entering the UK, which are not covered by the UK ETS.

To comply with the UK CBAM, relevant importers will be required to submit a CBAM return to HMRC, with any liabilities settled at the end of each accounting period. It is proposed that the first accounting period would run from 1 January to 31 December 2027. From 2028, the government proposes that accounting periods become quarterly.

|

Comparison: The UK mechanism would be different from the EU CBAM, which involves the purchase and surrender of ‘CBAM certificates’ at the current ETS market price. The government considers this model would be administratively more complex and may not accurately reflect the cumulative impact of other schemes like the Carbon Price Support (CPS), which adds an additional tariff on electricity generation, or the Energy Intensive Industry (EII) Compensation Scheme, which operates alongside free allowances. |

3.2 What would be covered?

The UK CBAM will initially apply to a specified list of commodity codes across seven sectors (aluminium, cement, ceramics, fertilisers, glass, hydrogen and iron/steel), which form part of the intent to focus on key carbon-intensive industries where the environmental justification is sufficient and can be weighed against the increased compliance burden on businesses. A full list of the intended in-scope products are set out in Annex A of the 2024 Consultation. This list will be kept under review on an ongoing basis. In-scope product codes would not be entitled to any exemptions.

Sectors in which there are challenges ascertaining the necessary data or where there are clear routes for circumvention have also been excluded for the time being but may be brought into scope if there are changes to a sector risk profile or where methodological or technological advances justify it. At the outset, there will be no perfect symmetry with the sectors covered by the UK ETS.

Scrap aluminium, scrap glass and scrap iron and steel have been provisionally excluded from the scope of the UK CBAM on the basis that (i) recycling the use of scrap goods has a net benefit on emissions (avoiding additional production) and (ii) there are methodological uncertainties around the calculation and attribution of emissions embodied in such goods.

The UK CBAM will be applied to ‘precursor’ product emissions embodied in imported CBAM goods for alignment to the UK ETS, although the precise goods to be deemed ‘precursor goods’ remain to be specified. A ‘precursor good’ is a good which is used as an input material in the production of a second good.

‘Direct’ and ‘indirect’ emissions will be subject to CBAM rates (replacing the ‘Scope’ terminology followed in the 2023 Consultation). Indirect emissions primarily relate to the emissions produced by the generation of electricity which is used in production. Aligning with the UK ETS, all embodied emissions in CBAM-covered imports will be measured in tonnes carbon dioxide equivalent (tCO2e).

|

Exceptions: Proposed exceptions to the UK CBAM covered sectors include phosphorus and potassium-based fertilisers, waste and scrap aluminium, iron, steel and glass and certain iron compounds. The proposed UK CBAM covered products are broadly consistent with the products listed in the EU CBAM, although the UK CBAM will also apply to glass and ceramics; the EU CBAM does not cover these products. Further and significantly, the EU CBAM applies to electricity, but the 2024 Consultation does not currently include this sector. |

3.3 Who will pay?

It is acknowledged that multiple persons may be involved in the import of a product and ownership may change during customs. For the purposes of UK CBAM, the responsible person will be either: (i) where customs controls apply, the person responsible for the goods when they are released into free circulation, or (ii) where there are no customs controls, the person on whose behalf the goods are moved to the UK.

3.4 When would the liability arise?

The government proposes that the “tax point” (when the UK CBAM liability arises and the rate is determined) will be either: (i) where customs controls apply, the date on which the good is released into free circulation, or (ii) where there are no customs controls, the date on which the relevant good first enters the UK.

If a relevant good enters the UK and is subsequently processed into a different good to which UK CBAM would not apply, it would still be captured by UK CBAM at the tax point.

The 2024 Consultation proposes a minimum registration threshold of £10,000 (looking at the aggregate total value of all CBAM goods imported) over any rolling 12-month period. Registration will be triggered by the earlier of (i) exceeding the threshold with a look-back over a rolling 365-day period, or (ii) the date which they expect to exceed the threshold on a look-forward to the next 30 days, with CBAM liabilities accruing from that date.

|

Reporting thresholds: The threshold for UK CBAM reporting (on an actual 365-day look-back basis, and on an expected, 30-day look-forward basis) will require businesses to institute monitoring and reporting systems on embedded emissions in relevant UK imports to demonstrate that they have assessed their eligibility for CBAM registration, should they achieve a potential £10,000 value threshold for all CBAM goods imported over any rolling 12-month period. |

4. How will the UK CBAM be calculated?

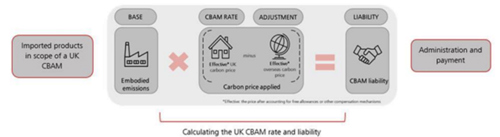

The applicable UK CBAM rate applied to the direct and indirect embodied emissions will reflect explicit carbon pricing in the UK and adjust for free allowances and other reductions to the carbon price paid domestically (to create a level playing field), as well as carbon taxes paid overseas in respect of the product (to avoid double penalisation in respect of the same emissions).

A diagram setting out the calculation of UK CBAM appears in Figure 1 below.

4.1 The UK CBAM rate

The applicable UK CBAM rate will apply per tonne of embodied emissions attributed to CBAM goods, with seven individual UK CBAM rates for each in-scope sector of goods. Accordingly, importers will need to declare the weight of the CBAM covered good, net of packaging, on their CBAM return.

The UK CBAM rate will be set by the government at the beginning of each quarter and will reference: (i) the average of the relevant sector's UK ETS auction price over the preceding quarter; (ii) an adjustment to reflect the existence of free allowances available to the domestic industry within that sector over the previous year (to be phased out in accordance with the phase out of free allowances); and (iii) the carbon price support rate for the current quarter.

These factors would be applied on a weighted basis to reflect the proportion of emissions that are either direct or indirect in that sector to produce a single blended rate (see Figure 2).

|

Rates and embedded emissions:

|

4.2 The taxable emissions

The government proposes that the methodology for measuring actual embedded emissions to which the UK CBAM rate will apply should align with and build upon existing rules set out for use by stationary installations within the UK ETS,[6] with specific details to be published at a later date

Independent verification principles applicable to the UK ETS will also apply to the UK CBAM, performed by members of the International Accreditation Forum (IAF), such as the United Kingdom Accreditation Service (UKAS).[7] Physical inspection of premises would form part of the verification process, and record-keeping would need to be sufficient to enable an external audit.

|

Key differences between UK CBAM and EU CBAM:

|

4.3 Offsetting overseas carbon liabilities

An importer can evidence an explicit carbon price (being a price/tCO2e placed directly on GHG emissions, via an emissions trading scheme with a market-based price or a carbon tax with a fixed price) imposed overseas in respect of the same embodied emissions to reduce its UK CBAM liability. This reduction would also be adjusted for local support mechanisms or free allowance equivalent which were available.

It is not clear to what extent the total liability for UK CBAM can be offset in this way (see Figure 3).

5. Alignment of reporting standards across the UK carbon regimes

A further UK government technical consultation is expected in 2024 with regard to establishing voluntary product standards to help promote low carbon products to consumers and to develop an embodied emissions reporting framework. Although demand-side reporting will not initially be aligned with the UK CBAM and current Scope 3 emissions reporting, the government has expressed an intention to align reporting metrics where possible.

6. Administering the CBAM

6.1 Submission of returns

To comply with the UK CBAM, relevant importers will be required to submit a CBAM return to HMRC, with any liabilities settled at the end of each accounting period. Once registered, if there are no CBAM liabilities, a ‘nil return’ would still be required.

It is proposed that the first accounting period would run from 1 January to 31 December 2027, with 30 May 2028 as the deadline for submitting the first CBAM return to HMRC with payment covering first accounting period.

From 2028, the government proposes that accounting periods become quarterly, with UK CBAM accounting periods ending on 31 March, 30 June, 30 September and 31 December. UK CBAM returns (and accompanying CBAM settlement payments) would then be due by the end of the succeeding month (30 April, 31 July, 31 October and 31 January) with the exception of Q1 2028, for which would be extended to 30 June 2028 to avoid a clash with the 2027 annual return deadline.

By 2028, the government expects eligible importers to have established processes with their suppliers for obtaining information about the carbon content of liable goods and the overseas carbon price on those goods as well as verification systems in place.

6.2 Penalties for non-compliance with reporting requirements

It is proposed that HMRC will have similar enforcement and inspection powers to those that are currently used to administer other taxes, including power to compulsorily register a liable person as well as to compel a person to provide information and documents necessary to enable HMRC to verify returns and assess liabilities for UK CBAM.

The government proposes to align with the penalty points system introduced for VAT for any late submission of returns or late payment. For each late return, there will be a penalty point until a penalty point threshold is reached. For VAT, if the threshold of penalty points is reached, there is a £200 penalty (with a further £200 penalty for each subsequent late submission while at the threshold). Penalty points can be removed/reset only in certain circumstances.

There will also be a general penalty for any non-compliance specific to CBAM, such as failure to keep appropriate records, late registration and failure to provide information.

7. International obligations

The 2024 Consultation notes that the UK CBAM is intended to be compliant with the UK’s World Trade Organisation (“WTO”) obligations, however (as noted in our publication on the EU CBAM) several countries have already expressed concerns about the EU CBAM, and are considering bringing WTO disputes against the EU. The structure of the UK CBAM (as a direct tax, rather than a surrender of certificates) might raise additional WTO compliance issues (particularly in relation to ‘national treatment’ obligations), if the carbon prices imposed on UK-produced goods differs from that of non-EU produced goods.

The UK CBAM could, similarly, be accused of having discriminatory impacts as importers will likely seek to shift the compliance burden, and the tariff cost, onto third country exporters. While it is likely that trading partners with more developed carbon regimes, like the EU CBAM, will seek to establish equivalence of eligible domestic carbon policies to avoid the UK CBAM, less sophisticated trading partners may suffer more as a result – although that is consistent with the aim of the UK CBAM to avoid ‘carbon leakage’ and arbitrage in jurisdictions with less environmental compliance infrastructure.

8. Conclusion

With the first UK CBAM accounting period starting from 1 January 2027, importers of CBAM-applicable products will need to start considering how to gather emissions data requirements and contracting with independent verification bodies who may be increasing demand. While the proposed UK scheme currently appears to be compatible with the UK ETS and the EU CBAM reporting requirements, to the extent there are further divergences between regimes and accepted methodologies this may result in additional cost and compliance burden. More detail will be required to determine the pricing and ability to offset for overseas carbon pricing.

Please get in touch with the authors or your usual contact at Slaughter and May if you would like to discuss any of the issues raised in this publication.

[2] UK Government, “Introduction of a UK carbon border adjustment mechanism from January 2027: Consultation”, 21 March 2024, available here.

[3] Samantha Brady, Samah Shah, Oliver Moir, Aaron Wu, Daniel Mewton, and Helena Cameron, “The EU Carbon Border Adjustment Mechanism Begins to Bite”, Slaughter and May Insights, 14 November 2023, available here.

[4] “Consultation Paper on Introduction of a UK carbon border adjustment mechanism from January 2027”, 21 March 2024, available here.

[6] As set out within The Greenhouse Gas Emissions Trading Scheme Order as modified from time to time, and the Monitoring and Reporting Regulation (Commission Implementing Regulation (EU) 2018/2066 of 19 December 2018).

[7] This is consistent with the Verification Regulation 2018 (Commission Implementing Regulation (EU) 2018/2067 of 18 December 2018 as modified as applicable to the UK ETS.